Unified content supply chain to drive Universal ecosystems value proposition

In today’s borderless multi-screen TV & video era, hyper localized digital audience preferences are pushing majority of media enterprises to build or create an unlimited value chain of content repositories across both live and VOD (Video on Demand) assets. This has gradually paved way for enterprises to embark on the content aggregation journey to enable not only to lower churn but also acquire newer niche customer base within both regional but global markets. Although, the aggregation ecosystem results into significant engagement rates, and exploiting newer monetization avenues but also have multifold increased the content supply chain complexities. Traditionally, media enterprises have followed a “best of breed” technology procurement lifecycle i.e., deployment of siloed architecture led on premise (prerequisite infrastructure costly) or cloud (lift and shift) technology stacks, resulting into creation of inefficiencies, higher maintenance, and support costs on the long-run basis. Furthermore, as multi-faceted aggregation (single asset, end to end OTT application, or multiple services bundling) becomes the new norm, this paves way for unification of content supply chain to not only increase operational productivity but also safeguard competitive edge (via protecting brand equity losses). Omdia’s ICTEI survey 2020/21, highlight that slightly more than two-fifth (41%) of media enterprises globally, unified content supply chain operations are the leading business priority in the next 18-24 months. Furthermore, majority of media technology vendors have diversified (through both organic and inorganic modes) their capabilities and functionalities building a vertically integrated ecosystem woven around a single workflow across the content supply chain. Couple of examples are:

- Verimatrix acquisition of Inside Secure to enrich its offering within application shielding etc. along with expanding footprint into IoT and connected car segments

- Rightsline purchase of Real Software to strengthen financial and royalties’ functionalities along with extending penetration into newer markets such as gaming, publishing, consumer products, life sciences and high tech

- Akamai building in-house capabilities around security (SOCC), and web performance acceleration (MPulse) to deliver a unified ecosystem woven around media distribution

- Brightcove and Ooyala together creating a vertically integrated online video delivery ecosystem value proposition, and

- Recently Limelight purchasing Edgecast to improve edge-based video distribution workflow competencies along with exploiting newer opportunities within cloud security and enterprise CDN space

- Encompass acquisition of Babcock’s media services to accelerate its playout services ecosystem and penetration within EMEA market.

Thus, it can be witnessed from the above that converging multi-dimensional content supply chain is an impeding push both from buy (enterprises) and sell (media technology vendors and ICT service providers) side across the media & entertainment segment.

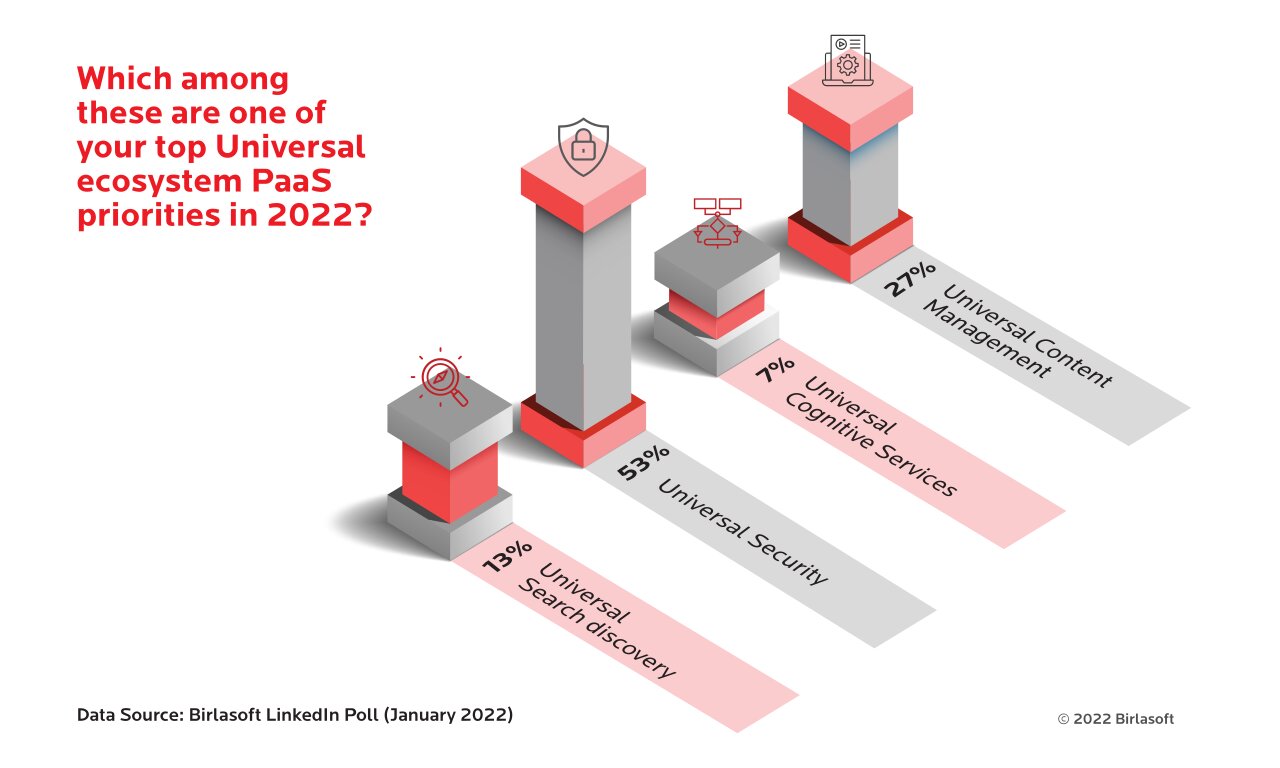

PaaS one of fast emerging cloud delivery mode lies at the epicenter of Universal ecosystems

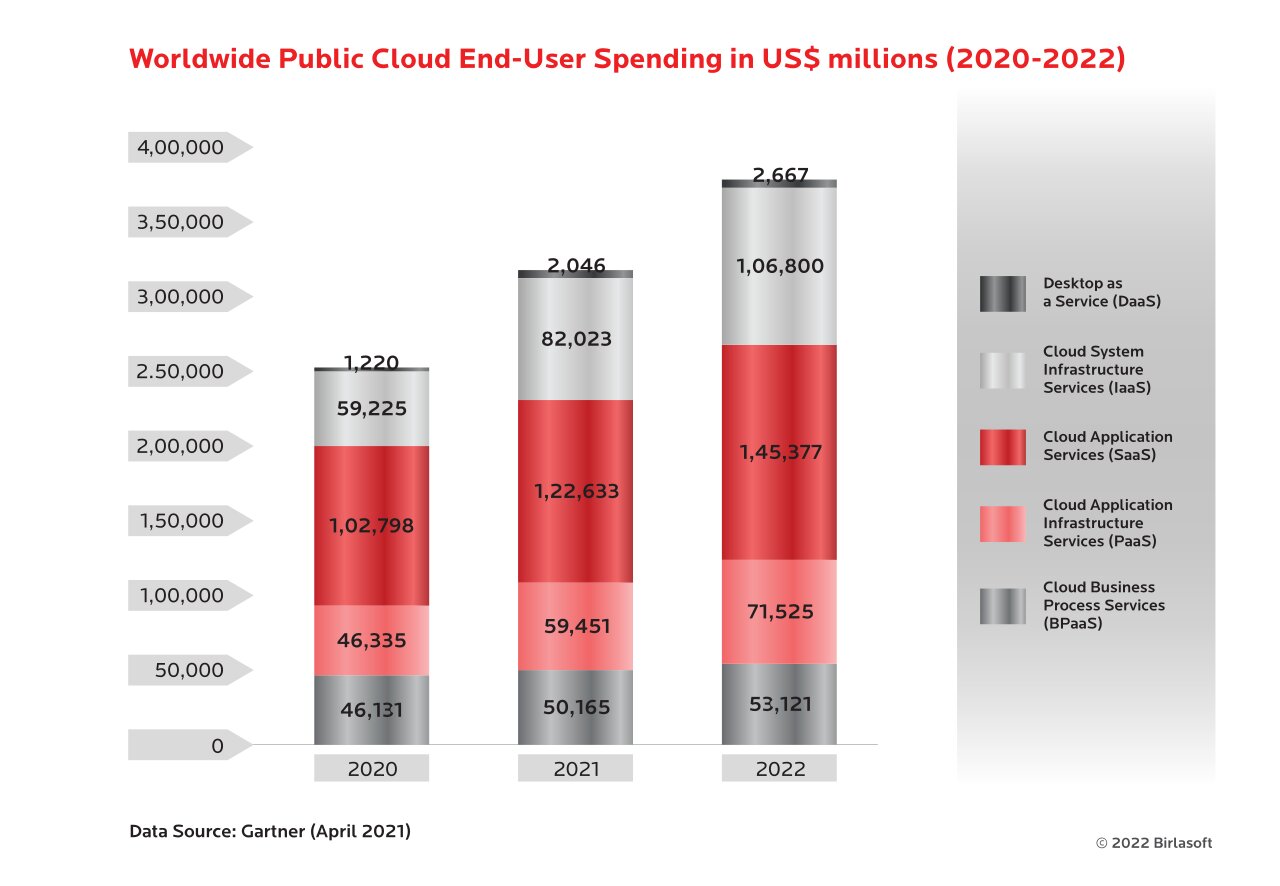

Gartner estimates that worldwide public cloud spending to US$398bn, with year-on-year growth of 20% in 2022. Although, Software as a Service (SaaS) will remain the largest segment accounting for almost two-fifth (37%) of total spend, it will register a slower growth of 19% as compared to the overall (21%). Platform as a Services (PaaS) will retain No 3-positioning controlling 18% of total spend but will witness strong annual growth of 25% by 2022.

Click to zoom in

In the M&E space, PaaS deployment mode is estimated to exceed both SaaS (+28%) and IaaS (+32%), with an annual growth of 39% in the next 12-18 months. Also, building Universal ecosystems on PaaS deployment configuration will also be prominent attributed to:

Key characteristics (Pull)3

|

Reference to Universal ecosystems (Push)4

|

|

Negligible need for owning and installation of in-house hardware and software to run applications

|

Managed multi-generation horizontally integrated applications across a single ecosystem (e.g., content management) via best-in-class technology vendor

|

|

Customization and lower administration TCO

|

Each ecosystem demand bespoke customization and ease of tangible and intangible complexities mitigation (centric to both resources and costs)

|

|

Pre-packaged horizontally integrated services, and solutions without managing back-end infrastructure

|

Single one stop multi-dimensional services across a single workflow without need for focusing on maintenance, upgradation etc.

|

|

Faster shorter lead-time-based deployment of newer applications to meet changing business requirements (COVID anti ripple effect)

|

Real-time, cost effective, on-going access of newer applications and solutions within a single agile ecosystem

|

- Pull is defined here as inherited characteristics or benefits of a PaaS cloud deployment configuration

- Push is defined here is benefits of a PaaS centric Universal ecosystem for media enterprises and their IT departments/engineers/developers assisting them to meet the business priorities

Thus, as media enterprises embark on the aggregation journey to create a localized personal ViewPlace

5 for each audience base will eventually acceleration the adoption of Universal ecosystems across the content supply chain in the next 2-3 years. This is pivotal due to bundling of multi-faceted assets, OTT services and in future non-media digital services within a single super offering will demanding:

- Streamlining of the operational media value chain ecosystem, and

- Tight integration with diverse external third-party content owners and aggregators.

{kind=link}

{kind=link}