AI and automation are the insurance industry's future and are already impacting it in several ways. Artificial Intelligent & automation can deliver on industry expectations by moving the mountains of structured and unstructured data and automating several insurance processes such as underwriting, claims to process, and fraud detection, to name a few.

Image

There is a lot of buzz in the industry about what automation can and cannot do, especially when it comes to Insurance underwriting. One area where this is true is if AI coupled with automation will genuinely assist in accelerating the underwriting process.

Let's clarify some common prevailing myths around AI and automation in insurance underwriting.

Myth 1 - AI and Automation will take away Underwriters’ Jobs

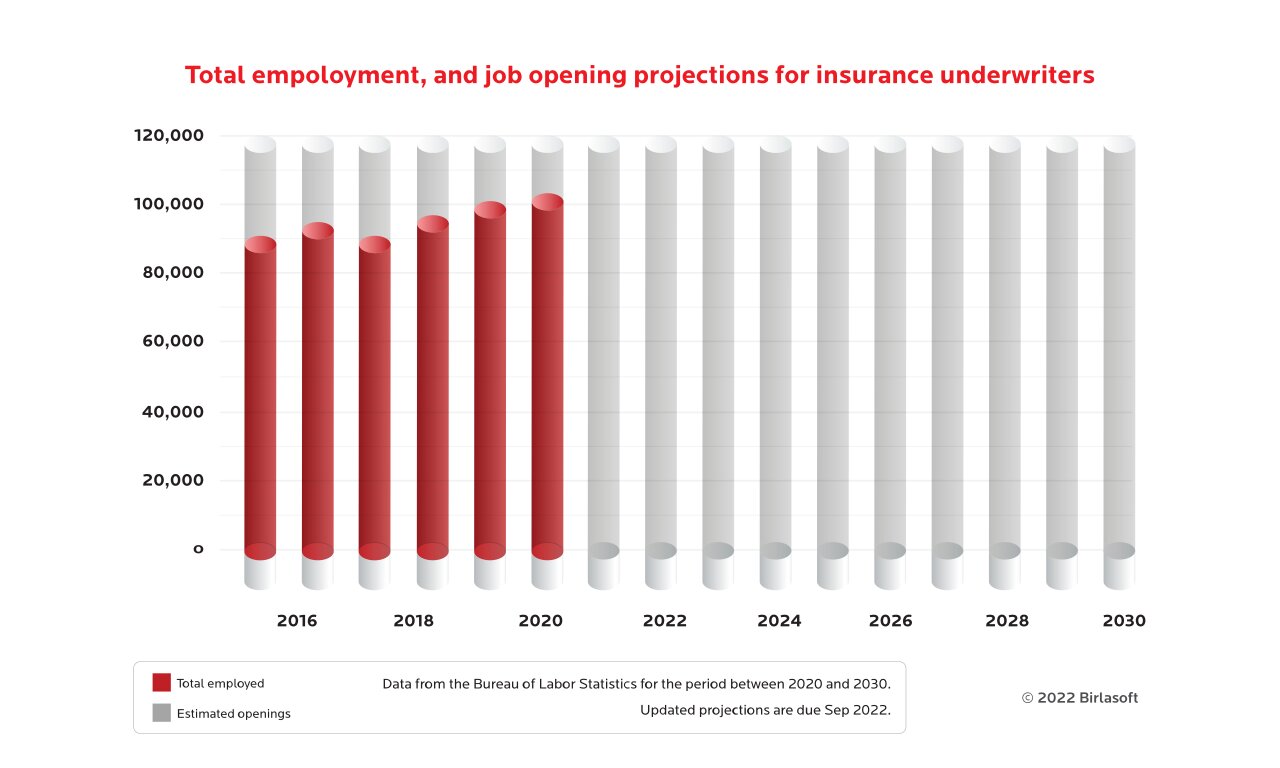

The fear that AI and automation will replace humans at jobs is not new! This fear and misconception are prominent among insurance professionals too. The fact is that AI and automation do effect jobs, but they are not here to replace humans but to assist them in doing a specific task, like file data processing, by feeding tons of data and letting it learn from that data.

Research shows that while there will not be an evident increase in underwriter openings, they will still be in demand. The demand for underwriters will decrease by -1.80% after 2030. In the future, automation will handle most of the claims, and AI will narrow the other tasks like scanning the documents faster. In contrast, human claim handlers will focus on other complex cases and- will have analytics to help them taking data-driven decisions.

AI-driven efficiency can make the tedious tasks & the process simpler, making the decision-making process more efficient. Insurance Professionals can focus more on the things that need a Human touch. However, the machines do take over some jobs and create new ones.

Myth 2: AI is Always a Black Box - harder to interpret

The uncertainty around AI and what it can offer has been a hot topic in the past few years. Many people wonder what this technology can do for them, but they may not know where to start. There are different types of AI algorithms, and each one has its own unique set of benefits.

As insurance industry adopts AI and Automation, it will become essential to focus on eliminating the risk of bias especially with the use of data that can be biased.

Many companies are already using it to predict risk, and AI will continue to make that process more efficient, accurate, and cost-effective. In addition, AI can help you with several things in your underwriting process. One of the most important ones is risk assessment. It can help identify which claims are likely to be fraudulent and filter out those that aren't—saving time for you and your customers.

The National Association of Insurance Commissioners (NAIC) has adopted 5 guiding principles on AI focussing below 5 key tenets:

- Fair and Ethical

- Accountable

- Compliant

- Transparent

- Secure/ Safe/Robust

Myth 3: Underwriting using AI and Automation costs a fortune

Many organizations think that AI is too expensive for small businesses. However, it is essential to know that underwriting using AI and automation can save you time and money. The traditional way of underwriting a loan can take up to 20 days or even longer. With automated solutions, you can get the same results in less than 24 hours. Research from Gartner says that 75% of customers expect a fast response to their claims, eventually increasing the insurance company's profits for a few key reasons:

1) Automated underwriting systems do not need to be trained on every type of risk, unlike human underwriters. Instead, they can be trained on a smaller number of risk types and then apply that knowledge to all other risks.

2) In today's fast-paced world, where companies need to be able to respond quickly to changes in their business environment or customer needs, downtime becomes highly critical. Automated underwriting systems can be used 24 hours a day, seven days a week, which means less downtime for maintaining the system or performing maintenance tasks.

3) Automated systems are also better at-risk mitigation because they can consider a broader range of factors than a less experienced underwriter.

Myth 4: Underwriters don’t need AI

Most Insurance companies have a lot of Data. This data comes from multiple sources, in multiple formats – Excel files, PDFs, Images, Word documents. Incorporating semi structured or Unstructured data into Enterprise pipeline can be a hassle without the right program.

Manual data management from ACCORD forms or brokers emails, piles of paperwork, seeking clearances, and tracking mail exchange with insurance brokers and customers can negatively impact your risk assessment process, pricing, and profits.

AI and automation optimize the underwriting process and not just decrease the operational costs but also enhances customer satisfaction by speeding up decision-making for underwriters. AI makes possible to overcome the challenges of unstructured data with speed & ease.

Myth 5: Not enough data to use automation in insurance underwriting and automation

You might think that there isn't enough data to implement automation into your insurance underwriting processes, but it's less likely to be that way. Instead, internal data will be more organized to enable and support the agile development of analytics insights.

The following are some types of ideal datasets:

- Customer Data (Demographics such as age, gender, or marital status)

- Purchase History (Information such as what products have been purchased by customers)

- Geographical Location (Customer’s location)

The AI systems are capable and efficient in drawing data from multiple sources and the algorithms can easily analyze these data points to determine whether an applicant should be approved or declined for coverage.

Myth 6: Automation isn't accurate

It takes months of training for an individual to learn how to use historical data from thousands of applicants who have applied for loans. Still with manual underwriting the errors often go unnoticed because they are challenging to identify and track. But with automated underwriting processes, you can set up alerts to notify you of any errors and fix them quickly with ease.

Automation is highly accurate in comparison to manual underwriting. It reduces claims errors and omissions (E&O), which means less paying out in claims and a higher customer satisfaction rate.

Myth 7: Automation can't handle complex cases

An automated system can help provide a more streamlined service for complex cases since it can mine through data faster than humans and suggest the most efficient solution for the customer's issue. Automated underwriting can take on a lot more than you might think.

With advances in artificial intelligence (AI) and automation, banks can employ algorithms alongside human under6writers to handle complex cases without sacrificing quality control. These programs can analyze large amounts of data quickly and accurately, allowing them to make decisions that would otherwise be impossible for humans alone. In addition, they can also offer personalized recommendations based on past experiences with similar clients, which allows them to provide better service.

In many cases, AI can help with these complex tasks by automating parts of the process and providing human agents with data-driven insights.

What insurers need to know

The pandemic lit a fire under many insurance companies, forcing them to adopt digital transformation at a much faster speed than previously planned.

The insurance industry has been plodding to embrace innovation, and insurers can no longer afford to ignore AI and automation as an integral part of their business models.

The future of insurance holds a place where artificial intelligence and automation will do various tedious tasks, including fraud prevention, risk assessment, and analyzing claims. With advancements in data analytics, artificial intelligence (AI), and automation evolution, more companies will adopt these technologies in their underwriting processes.

Why should you opt for automation in insurance?

The AI and automation in insurance industry are here to stay and every organization will gradually be forced to embrace it. As the insurance world changes and grows, it is essential to stay one step ahead. According to a PwC survey showing the widespread adoption of AI says that 54% of the insurance companies are already implementing AI and are looking to scale up. AI-driven systems and intelligent automation have made their way into most industries, allowing businesses to reduce costs, streamline processes, and improve efficiency. Insurance is no exception.

How Birlasoft can Add value in AI-empowered Insurance Processing

Birlasoft’ s submission automation solution will optimize your underwriting process for you and will keep you one step ahead of your competitors.

Recommended

{kind=link}