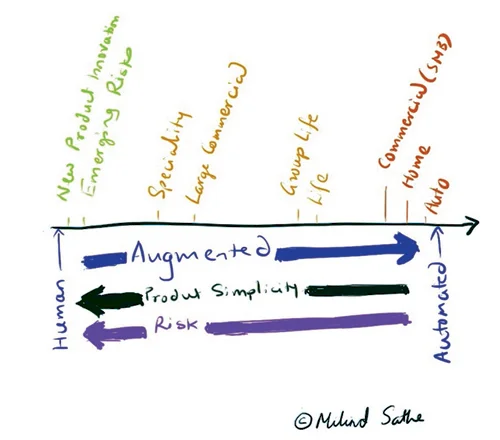

Augmented Underwriting is an evolving step from fully human underwriting to automated underwriting.

Simpler products like Auto, Home and Commercial (small & medium business) have already been mostly automated. IoT sensors (think UBI: Usage Based Insurance), data modeling (data science) and other newer inputs are making this automation more efficient.

More complex products like Specialty Insurance, Large Commercial, Life are not yet automated but the underwriting is augmented with ML and data science. The rating derived from these models are fed to an Underwriter as an input. The Underwriter makes the final determination.