In light of this, spending on cybersecurity training is expected to reach $10 billion by 2027. As cybersecurity threats increase exponentially, so do the number and extent of the regulations that are aimed to protect organizations and their customers, which ultimately puts pressure on the CISOs to keep track of fast-changing cybersecurity regulations, and at the same time, maintaining a strict vigil on third party suppliers. Such risk assessments are often time-consuming and mundane activities for CISOs.

Additionally, manual approaches to counter such threats could make companies more vulnerable. AI and automation are increasingly becoming enablers in the regulatory risk value chain to simplify and speed up cybersecurity compliance. An effective AI-enabled cybersecurity program allows these organizations to protect their critical assets while ensuring they are fully compliant with the cybersecurity regulations laid by government entities.

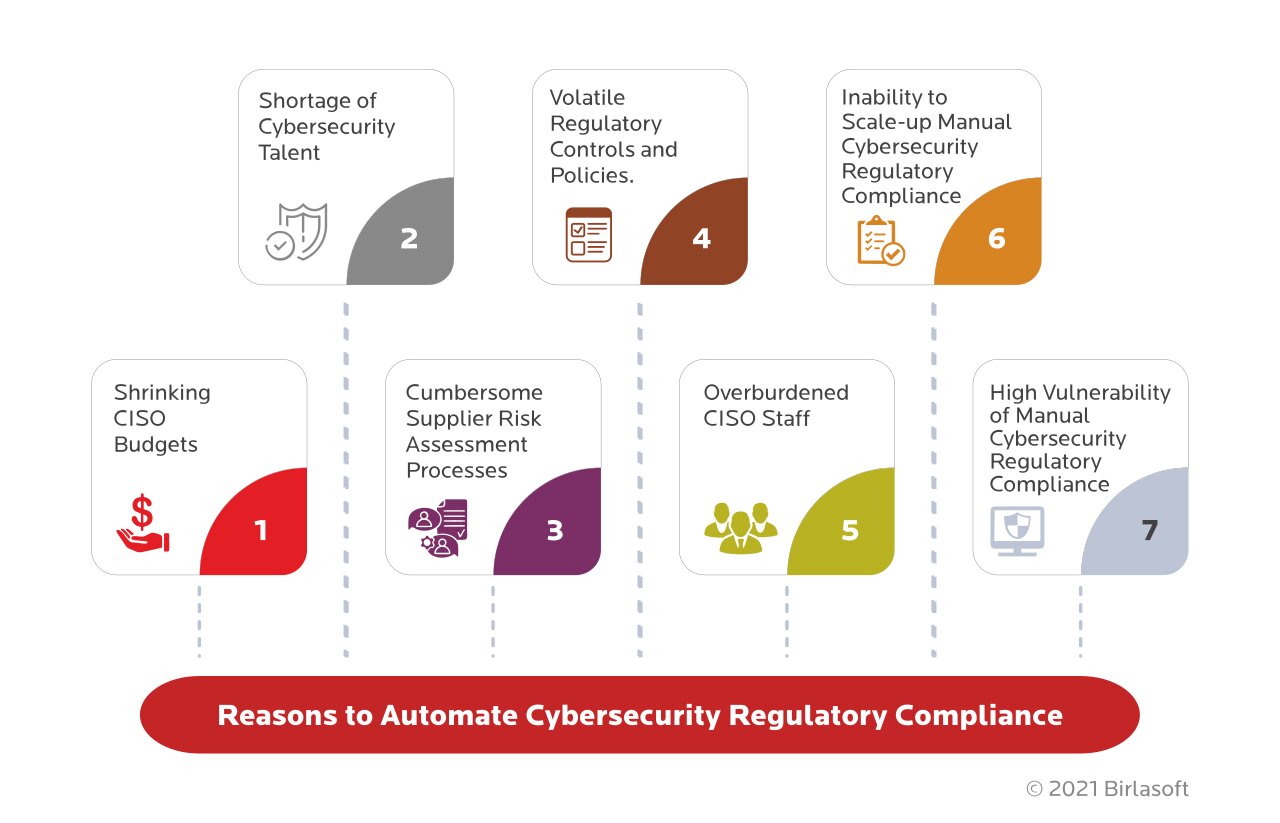

Reasons to Automate Cybersecurity Regulatory Compliance

Talk to the audit managers about the cumbersome manual cybersecurity regulation compliance process, and they will be quick to recognize the need for automating these processes. For audit managers, manual testing proves to be inefficient and doesn't provide enough data on the operating effectiveness of controls. In such a scenario, automating the regulatory compliance process makes sense as it dramatically improves efficiency and frees up time to invest in cyber resilience, which otherwise suffers .. Besides, automation also significantly reduces costs associated with the high volume of manual effort. Let's look at seven such factors in more detail.

#1 Shrinking CISO Budgets

A recent study by McKinsey stated that more than 70% of CISOs surveyed report that their budgets for the fiscal year 2021 have shrunk owing to the Covid-19 pandemic. This has led to a limited outlay for compliance, governance, and risk tools. Additionally, for corporate security operations centers, the cost of securing the fundamentals could further limit the budgets for more sophisticated threat-intelligence upgrades, behavioral analytics, and other tooling.

In line with this, automating routine tasks helps free up employees' time for other value-added work. The CISOs' resilience during the Covid-19 pandemic has shown the path towards automation, as highlighted by this Deloitte study. CISOs in the financial services industry are deploying emerging technologies such as cloud, data analytics, and Robotic Process Automation (RPA) as top cybersecurity investment priorities. This was done to emphasize access control, protective technology, and data security. These technologies present new solutions for financial institutions to transform operations and achieve cost reductions eventually.

#2 Shortage of Cybersecurity Talent

The intense focus on cybersecurity highlights the necessity of creating a secure base for digital businesses that shields their organization and clients. This Gartner survey indicates that in most enterprises, the CIO still owns the responsibility for cybersecurity. However, the IT organization alone can't provide cybersecurity anymore; business colleagues must be engaged.

Investing in software that can analyze risks in real-time as well as automate some of the risk assessment processes aids companies in mitigating the problem of talent shortage. This will also substantially reduce the demand on operating security budgeting, allowing organizations to hire security experts for jobs that will have a high return rather than letting them work on outdated legacy processes.

By automating the risk assessment process, the cybersecurity professionals wouldn't need to go through various assessments manually, saving time and cost. Additionally, automation would also make the processes more efficient, allowing businesses to reallocate resources to address other pressing requirements.

#3 Cumbersome Supplier Risk Assessment Processes

A survey by the Ponemon Institute recognized the increasing threat of cybersecurity breaches from third-party vendors. To mitigate these data breaches caused by poor risk management practices, it is prudent to monitor the vendor's cybersecurity situation. Additionally, organizations must understand that once a third-party vendor encounters a data breach, the larger organization is more susceptible to a cybersecurity breach. In view of this, a well-orchestrated vendor risk assessment helps protect the entire business ecosystem from exposure to cybersecurity gaps created by vendors organizations share data with.

This can only happen through automation. Bringing in the organizational hierarchy involved in vendor governance enhances transparency and improves accountability in various departments such as Supply Chain Management (SCM), Risk Management and Mitigation, Compliance Management, Procurement, and Quality. It also addresses gaps or loopholes in the organizational hierarchy to mitigate any potential risk. In short, technology adoption helps companies map vendor risks to the associated regulations, controls, internal stakeholders, and vendors, resulting in improved risk transparency and accountability.

7 Reasons for CISOs in Financial Services to Automate Cybersecurity Regulatory Compliance

{kind=link}