Automated underwriting also significantly enhances loan providers' profit margin from cost cuts in manual underwriting labor and improves customer satisfaction. If companies are looking for Automated Loan Underwriting, there are strong reasons to validate their belief. Automated Loan Underwriting enables digital verification processes throughout the loan cycle. It automates processing and underwriting events entirely as well as the document generation process and also allows digital delivery of the same. The process facilitates real-time integration of all associated parties with the loan origination system (LOS) for exchanging data between applications and introduces e-closing, recording, and vaulting options.

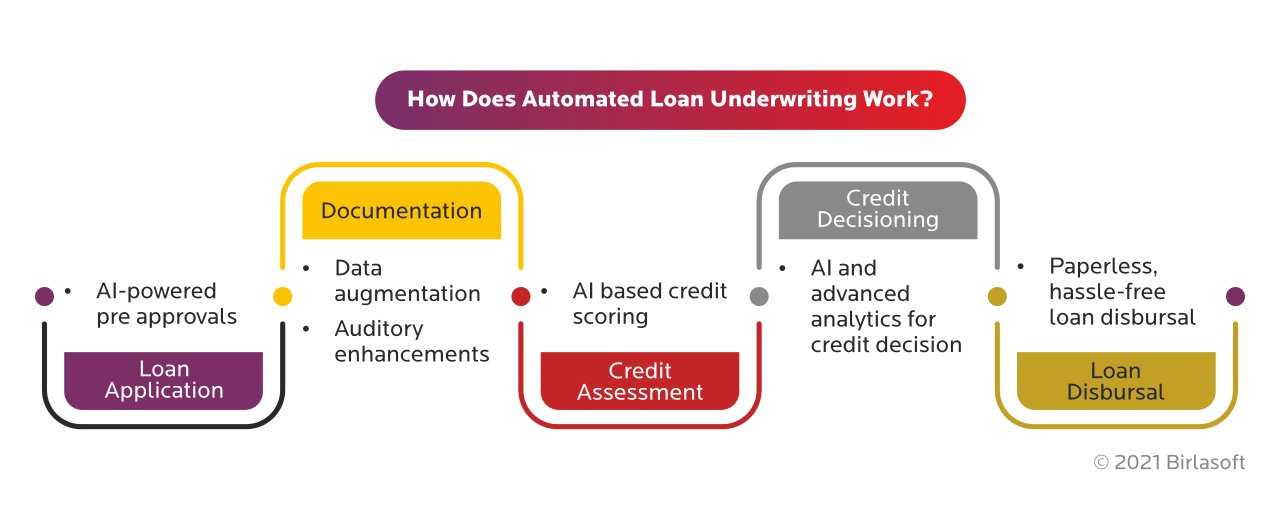

How Does Automated Loan Underwriting Work?

There are many technology tools available today in the market that are revolutionizing the lending sector globally. AI, ML, RPA, NLP, Optical Character Recognition (OCRs) are some of the few new-age technological advancements that genuinely possess the potential to bring a dynamic shift in the way loan approvals and disbursals are taking place globally.

For instance, with its ability to reduce loan-processing time by up to 80%, RPA is poised to transform the digital lending space, as is evident from its rapid adoption by fintech companies. RPAs significantly reduce human errors, automate mundane tasks, assist with regulatory compliance, enable significant cost savings, promise 24*7 support and lower the risk of cyber fraud.

In crux, RPAs expedite loan processing and disbursement and enhance the productivity of the workforce as well. Let's look at other such technologies that make loan processing a convenient and hassle-free affair:

Loan Application

When it comes to tracking and monitoring loans for defaulters, AI models monitor and track all the incoming payments and predict a loan default score that is updated over time. If a customer is identified as being at high risk of default, then the software prompts loan executives to draw out a different deal for such customers.

During a recent survey by CSA, it was found that mortgage companies are aiming to reduce the loan processing time from prequalification to closing. Their objective is to reduce cycle time by at least one day, with about 35% wanting the implementing process efficiencies to be sliced as much as five days off of the cycle time, and another 30% planning to shave off 6 – 10 days, while the other aspirational ones aimed to reduce cycle time by 11 days or more. The same survey also stated the impact that automation can bring and that 70% of respondents believe technology or automation is the solution to improve performance.

Documentation

Consumer mortgage lending has always been paper-intensive as it requires hundreds of documents to be generated for each application, which doesn't even include loan servicing documents. Such requirements arise due to the complexity of mortgage lending processes where organizations are dependent on multiple systems, databases, workflow tools, and reports throughout their operations, which mandates processors to access numerous resources to complete specific processes.

Managing such loans can be exceedingly resource-intensive without an intelligent automation solution in place. Automating such methods can help businesses manage documents and data, reading and compiling data pulled from several sources and in various formats such as third-party websites, PDFs, and email into a single view. Automation also enhances the audit capabilities of the lender, while encoding checkpoints into the bots will result in a faster and streamlined secondary review and testing.

How Does Automated Loan Underwriting Work?

Credit Assessment

The expanse of automation has made it possible for lenders to program their creditworthiness and risk parameters into an automation lending solution, thereby helping companies to move away from manual assessment, which is too time-consuming and, at the same time, error-prone. Automated mechanism even facilitates relatively inexperienced personnel to speedily screen loan applications, which in turn enhances customer service by providing a fast turnaround to loan applications.

Moreover, they allow a high degree of customization, and these standards can be set up for different types of loans, which comes in handy for small business lending as many small business clients may not fall under the gamut of conventional approval criteria. Besides, as another plus point, an automation lending solution allows the institution to devote its underwriters' time to applications that need further review, rather than having them process 'normal' loans that can be cleared via a programmed template. AI can assist financial agencies in determining borrowers' creditworthiness and reduce loan defaults using predictive analytics and NLPs.

{kind=link}

{kind=link}